The Top 5 Investment Mistakes Expats Make (and How to Avoid Them)

When it comes to losing weight, most agree that short-term fads don’t work. The only permanent solution is to maintain a sensible diet and exercise plan over time. And it's the same with investing. Get-rich-quick schemes or investments won’t work.

Despite all resources dedicated to making short-term investment predictions, the reality is that no one has the ability to consistently foresee the future. The truth is much more mundane: Long-term investing success rests on avoiding the big mistakes and by following a properly designed investment plan over time, and through all market conditions.

Here are some of the common investment mistakes that expats make, and how to avoid them:

1. Avoid Giving in to Greed and Fear

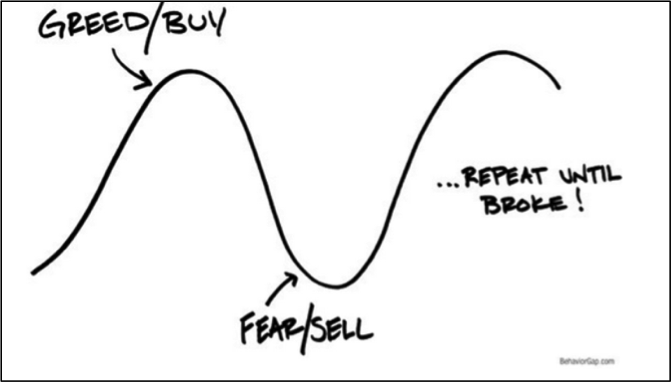

We're all susceptible to greed and fear, whether it's taking a punt on the latest hot biopharmaceutical stock, chasing tech stock returns, or hoarding cryptocurrency or gold bars to protect against the demise of the world's fiat currencies. And it's no wonder―with entire websites, online newsletters, and 24-hour TV channels touting the latest "can't miss" investment or impending financial catastrophe, it's easy to fall into a cycle of greed and fear.

The Cycle of Greed and Fear

Source: “The Sketch Guy” Carl Richards, CFP®, www.behaviorgap.com.

Unfortunately, this is the quickest way to investment ruin. Underlying the media's not-so-subtle emotional manipulation is the presumption that the future is predictable. It's not. Evidence has repeatedly shown that investors, as well as self-appointed prognosticators, are no better at foretelling investment outcomes than they are at guessing the winning number on the next roll of the roulette wheel. It’s not possible to predict which asset class will be the best or worst in any given year. Performances of each asset class changes dramatically from year to year, as shown below:

Source: Morningstar.

To avoid getting caught in the greed-and-fear cycle, ignore short-term market noise. Focus instead on the long term—remember that your long-term portfolio contains funds you'll use over the rest of your life. Build a diversified portfolio between a defined mix of different asset classes, and stick to it, rebalancing when the allocation moves outside of your long-term strategy.

2. Minimize Investment Product Fees

Ignoring investment product fees can wreck your portfolio returns. One to two percent may not sound like very much, but it can take a huge toll on your portfolio over time. All investment products charge fees for management, administration, marketing, and other administrative costs. In the offshore markets, expats are often paying a front-load fee of 5% or more and ongoing annual fees of around 2%. These fees are even higher for heavily marketed investment-linked insurance schemes, where the total ongoing fees can reach 4–5% per year.

When you understand that over the long run your portfolio is only likely to produce annual returns in the range of 6–9% before fees, you can see how much impact these fees can really have. Things look even worse when you consider inflation, which has historically averaged 3–4% (and higher in some emerging markets). After subtracting inflation, your portfolio is only likely to generate real returns in the range of 3–5%. This is the real growth your portfolio generates in purchasing power to keep up with the rate of inflation.

The fees directly reduce the inflation-adjusted growth of your portfolio. If your portfolio achieves a pre-fee average return of 7% per year and if inflation averages 3% during the same period, your average real return is only 4%. If you pay annual fees on your portfolio holdings of 2%, your real return is now only 2%. This means your portfolio is growing at only 2% on average in real or purchasing power terms. The fee in this case is like a 50% tax on your real investment earnings. Many expats are paying total fees on their investment portfolio well in excess of 2%, which means it will be very hard to achieve long-term growth in the portfolio.

Rather than paying high fees to access products, focus on getting proper investment and financial advice geared to your long-term financial well-being. Portfolios can be built on a global brokerage platform for a fraction of the cost of portfolios constructed from the typical investment products sold in the offshore markets. This low-cost access to products can be coupled with an advisory service that helps you devise and manage a globally diversified investment portfolio. The benefits of this approach are lower fees and ongoing advice aligned with your long-term interests.

3. Pay Attention to Taxes (Especially for Americans)

Right up there with not paying attention to fees is not paying attention to taxes. Some expats are lucky enough not to have their offshore investments taxed by either their home countries or countries of residence. Others, particularly Americans, are not so lucky. They will be taxed on capital gains, dividends, and interest no matter where they live.

Luckily, there are some options to reduce the impact of taxes, such as using available national tax-deferred and tax-exempt savings schemes or tax-deferred corporate pension plans (this does not include high-fee, insurance-wrapped investment structures). Additionally, investors can reduce the impact of taxes by selecting appropriate investments that generate tax-exempt interest or pay little in the way of distributions and by managing capital gains.

Used properly, tax management in a portfolio can decrease the drag on investment returns by as much as 1%.

You can't control the markets, but you do have some control over the amount of taxes and fees you pay on your portfolio. Any reduction in these two areas adds to your return without taking any additional risk. This is free money.

If your portfolio is earning a pre-tax, pre-fee return of 7% with inflation at 3% and you are paying 2% in fees on your investments and another 1% to taxes, your real return is only 1%. If you can reduce your fees to 1% and the tax burden through proper management by 0.5%, you will have increased your real return from 1% to 2.5%. While this doesn't sound like much, this can increase the value of the portfolio by more than a third over a 20-year period.

4. Avoid Currency Mismatch on Funds for Short-Term Goals

Most expats maintain a bias toward their home country. They tend to think in that currency and to overweight investments in their home country. For expats on short-term overseas assignments who intend to return to their home country, sticking to a home currency can work well. But for long-term expats or those planning to permanently remain overseas, sticking to your home currency may be a mistake.

The goal of any investment portfolio is to fund future expenses. For many expats, those expenses will be denominated in currencies other than their home currency. As we are all aware, currencies can be notoriously volatile. For shorter-term goals such as emergency funds or near-term living expenses, having a currency mismatch between funds intended for these goals and of your expenses can be a disaster. Longer-term goals such as living expenses in retirement may be best funded through a globally diversified portfolio that has multiple currency exposure, denominated in one trading currency.

5. Don’t Put It Off—Get Started

Procrastination is just as devastating to the success of your investment strategy as any of the above mistakes―maybe more so. It's easy to let life get in the way and assume you'll get to it later. The problem is that time rarely comes. This is particularly insidious for investments, as much of the future value of your portfolio is based on the compounding of returns over time. Devising and contributing to a properly designed portfolio early and consistently has a far greater impact on ending portfolio values than contributing a greater amount later on. Also, with today's uncertain job security, later on may never come.

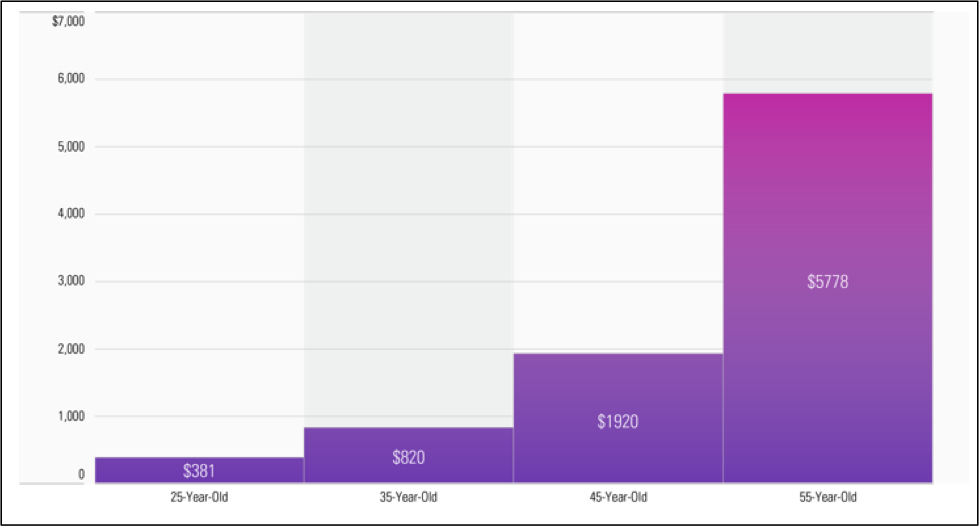

You may have heard the story of twins Bill and Phil. At age 19, Bill starts saving and investing U.S. $5,000 per year in an investment portfolio that earns an average 7% per year annual compound return. He stops contributing after just 10 years and lets the investment grow until he retires at age 65. Phil doesn't get started until age 31 but then contributes $5,000 per year to an investment portfolio that similarly earns 7% per year compound return. Phil contributes for 35 years until he retires at age 65. Who saves and contributes more? Who has a bigger portfolio at retirement?

Phil saves considerably more—$5,000 x 35 years = $175,000 in total—while Bill saves only $5,000 x 10 years = $50,000. Yet Bill still has more at retirement ($844,434) versus Phil's $739,567, simply because Bill got started earlier.

In Summary

Along with your savings, the returns you earn largely determine your ability to achieve your financial goals and financial security. You can't control the market, but you can control many other ways to increase your portfolio returns and reduce risk. Avoiding the mistakes above will go a long way to boosting your portfolio return and putting you on the path to financial security.

This article is a revised and updated version of one that had appeared previously on www.crevelingandcreveling.com.

Additional Resources:

Expat Case Study: Overcoming the Cycle of Greed and Fear in Investing

Expat Investment Advice: Don't Chase Returns; Diversify Instead

Expat Investment Advice: Tips for Dealing with Market Volatility

Expat Investment Advice: Seven Things Expats Need to Know About Investing

Smart, Low-Cost Investing for Asia's Non-U.S. Expats

Looking Past the Sales Pitch: Analyzing an Offshore Insurance-Linked Investment Scheme

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2020 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.