Expat Case Study: Overcoming the Cycle of Greed and Fear in Investing

Creveling & Creveling protects its clients' privacy. The following is a fictitious example designed to demonstrate the type of financial decision-making required to achieve financial security and does not refer to any specific case.

The Situation

Craig and Cindy are expatriates from Toronto in their 50s. Their two kids are grown, and the couple has been working to save, hoping to accumulate enough to retire when they reach their mid-60s. They’ve worked out that they need at least U.S. $2.5 million in today’s dollars to fund the kind of retirement they’d like to have. However, with most of their savings in low-interest fixed income investments or cash, and with interest rates at current levels, they wonder if they can ever accumulate enough to retire.

The Cycle of Greed and Fear

Craig and Cindy weren't always so cautious. Back in the mid-1990s, they enjoyed investing in the stock market. Through their broker, they bought shares in a number of “dot-coms” listed on the booming NASDAQ exchange in the U.S. As the market prices of their shares rose, they bought more until, by the end of 1999, the market value of their portfolio was just over U.S. $1 million. But then came the market crash after the turn of the millennium. They watched in horror as the value of their portfolio was cut in half, with many of their investments becoming worthless. The couple sold the remainder of their shares and vowed to be more cautious going forward.

Craig and Cindy spent the next few years saving as much as they could in low-volatility, fixed income investments. But after witnessing the stock market's strong recovery in 2003–2005, they had decided to begin buying stocks again by late 2006. This time, they decided to invest primarily in strong-performing emerging market stocks, as well as in buying an overseas property investment.

By late 2007, they had moved most of their savings into equity and had also made a deposit on an off-plan Spanish holiday home. But then came the global market crash of 2008. Their portfolio once again plummeted as fear and panic swept global markets, and the developer of their Spanish holiday home went bankrupt without finishing the project. Craig and Cindy cashed out of everything they could sell in early 2009, losing much of their principal investment. This time, they vowed to play it very safe going forward. In 2017, their savings remain in fixed income investments, although they're considering whether buying gold, Swiss francs, or a cryptocurrency fund would be even safer, or perhaps one of the high-fee, low-return "guaranteed" structured products that their friend's private banker has been pushing.

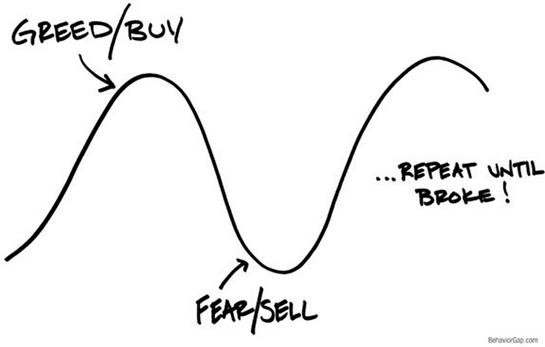

The Cycle of Greed and Fear

Source: “The Sketch Guy” Carl Richards, CFP®, www.behaviorgap.com.

The Approach

The problem starts with their (lack of an) investment strategy: Given their experiences, it's understandable why Craig and Cindy would want to steer clear of investing in stocks or other forms of volatile investments. From their perspective, equity investments seem unpredictable and unsafe. In steering clear of equities, however, they face a real problem: It's unlikely that they'll be able to save enough in cash and fixed income alone to retire on, and even in retirement, they’ll need to hedge against future inflation. How can they bridge the gap between finding investments that are safe in the short term and ones that will provide them with enough return to meet their longer-term goals?

First, they need to understand that the real problem with their investing thus far is that they have been simply chasing the latest trend or hot tip, instead of diligently following a strategy that works. Like many expats, instead of having a logical, strategic plan for saving and investing, Craig and Cindy have merely fallen prey to market noise, financial “news” programs and articles, and their emotions.

This is not unusual. The relatively new field of behavioral finance, which studies irrational financial decisions, teaches that as investors, our biggest priority is avoiding short-term pain (such as avoiding short-term losses), after which we seek short-term gratification (in spending more today or in speculative trading to try for a quick profit). We get sucked into short-term thinking and do not focus on longer-term issues such as how to accumulate enough to retire comfortably.

Furthermore, it's in our nature to pay more attention to entertaining sound bites from the media or a broker, rather than striving to understand complex concepts that really work. We also tend to believe that whatever has just happened will continue into the future. While it's true that some of these tendencies are derived from strategies that may have served mankind well in more primitive times, unfortunately they do not work for successful long-term investing.

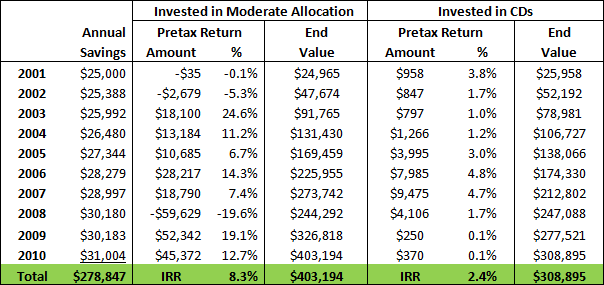

How following a long-term strategy produces different results: Once Craig and Cindy understand that the problem is in their emotions-based approach to investing, they next should see how following a solid long-term investment strategy would have compared with either staying in cash (their current strategy) or letting a cycle of greed and fear dictate their investing (their past behavior). For example, even in a notoriously tough period for equity investors such as 2001–2010 (sometimes called "the lost decade of investment"), annual savings consistently invested in a moderately allocated, globally diversified portfolio would have outperformed savings placed in certificates of deposit (CDs):

Results are before taxes and fund fees. Moderate portfolio allocation: 40% fixed income, 60% stocks and real estate. Annual savings increases annually by the average rate of inflation. IRR is the internal rate of return of the annual savings cash flows into each portfolio over the investment period. Source: MGP, Ibbotson & Associates, C&C estimates.

As shown above, even during the lost decade of investment, a moderately allocated diversified portfolio could have outperformed cash by a large margin.

And if you look back for longer periods, the case for following a disciplined strategy of annual savings and investing becomes even stronger. For example, had Craig and Cindy saved and invested in the above moderately allocated, globally diversified portfolio for the past 30 years (1987–2016), they might have achieved an average return of 8.2% per year versus just 2.2% per year for a portfolio invested in CDs. In this case, the final value of the moderate portfolio would be more than double (150%) the CD portfolio's value. To put some numbers to this, instead of having U.S. $1.6 million from investing in CDs for 30 years, they could have achieved nearly U.S. $4.1 million with the moderate portfolio. While investing steadily in precious metals might have achieved a slightly better return than CDs if they were able to stick with the extremely volatile asset class, the fact is most tend to buy this type of investment near the peak and sell after a collapse (creating the bubble):

Performance Over 30 Years (1987–2016): Moderate Portfolio, CDs, Precious Metals

Value of saving and investing $25K per year for 30 years ending December 31, 2016, invested in moderate portfolio (60% risky assets, 40% fixed income), CDs, and precious metals. Source: MGP, Ibbotson & Associates, C&C estimates.

The Solution

If Craig and Cindy can accept that they will need some equity investments to have enough money to retire and that short-term volatility in a well-diversified portfolio's value does not equate to long-term losses, they will be in a better mental position to move to a more disciplined long-term strategy that will work for them. To achieve their goals, they do not necessarily need to have an extremely aggressive allocation that will experience the highest amount of short-term volatility, but they should understand that even a moderate allocation may experience a loss in quoted value over any one- or two-year period.

As long as they don't get spooked and cash out their well-diversified portfolio when markets are most depressed (and ideally continue to add additional savings to it), they will come out ahead in the long run. Once they have a better understanding of how long-term investing really works, their next step will be to design a globally diversified portfolio using low-cost exchange-traded funds (ETFs) and mutual funds that suits their future spending goals and plans to continue living overseas. See “Expat Investment Advice: Seven Things Expats Need to Know About Investing" for more information on this next step.

This article is a revised and updated version of one that appeared previously on www.crevelingandcreveling.com.