Expat Financial Advice – Successful Investing for an Overseas Retirement

By Chad Creveling, CFA and Peggy Creveling, CFA

How much will you need to retire overseas, and how should you invest to achieve that goal? For many of us, a retirement portfolio the equivalent of US $1 million might seem to be more than enough - almost like winning the lottery. Unfortunately, US $1 million doesn’t go as far as it used to. Depending on your overseas lifestyle, this amount may provide only a reasonable, not generous, retirement – especially if it’s expected to last 30 years or more. In this article, we’ll explain how to judge if the equivalent of US $1 million will be enough for you, as well as how best to invest to ensure you don’t run out of money or have to curtail your lifestyle.

US $1 Million Can Buy a Reasonable - Not Affluent - Retirement

An often-quoted rule of thumb is that you should be able to withdraw an inflation-adjusted 4% per year from your retirement savings with a low chance of running out of money over a 30-year retirement. But even if you have saved US $1 million, 4% is only US $40,000 — less than the median income in the U.S., and less than some expat families spend on just travel and entertainment in a year. This amount doesn't quite purchase the type of lifestyle that you might expect for a millionaire.

Even then, depending on how you invest, there is a substantial risk of outliving your money.

Simplistically, just putting the money under a mattress and dividing the amount by 30 would give you about $33,000 per year.

But this doesn't take into account inflation. Thirty years of inflation at 3% per year reduces purchasing power by 59%. At an average inflation rate of 5% per year (not unheard of if you live in a country with an emerging economy), purchasing power is diminished by 77%. This means that $1,000 today would only buy you $412 worth of goods in 30 years with 3% inflation and just $231 with 5% inflation.

For your $1,000 to be worth $1,000 (able to purchase $1,000 of goods) in the future, it's going to have to keep up with inflation. The annual inflation rate in the United States has averaged 3.47% per year from 1979 to 2022

To Beat Inflation, Invest in a Diversified Portfolio

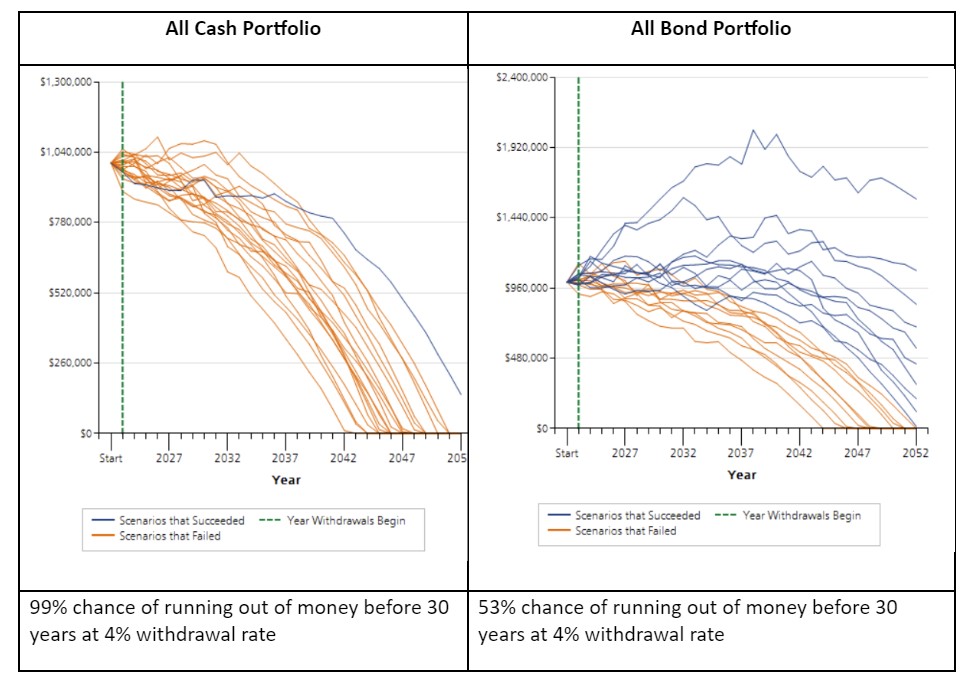

Unfortunately, investing in a cash deposit or money market account doesn't work much better than the mattress. An all fixed income (bond) portfolio is better, but not good enough. Our examples below show what happens to 1,000 potential 30-year return sequences for $1 million dollar cash or bond portfolio, subject to the long-term average inflation rate of 4.21% per year while withdrawing an inflation-adjusted, after-tax amount of $40,000 each year. Portfolio earnings are assumed to be subject to a 15% tax rate.

Is $1 Million Dollars in Cash or Bonds Enough for 30 Year Retirement at 4% Withdrawal Rate?

Note: Monte Carlo analysis, 1,000 iterations using different pathways of random actual returns

As shown above, the cash portfolio does not last for 30 years, and the bond portfolio only succeeds in about half the cases. If inflation is higher than average, the chances of both portfolios lasting for a 30 year retirement would be worse.

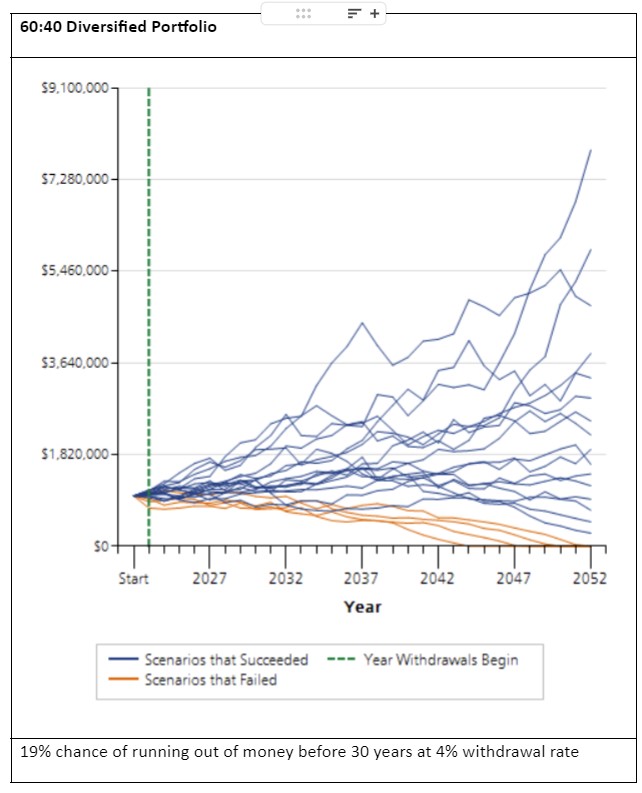

Contrast the above results with the same analysis, but this time using a portfolio diversified across various fixed income, equity, and alternative asset classes, with a split between equity-type risk and fixed income risk of 60%/40%:

US$1 Million Dollars in a Diversified Portfolio – Better Chance for 30 Year Retirement

Note: Monte Carlo analysis, 1,000 iterations using different pathways of random actual returns

As shown above, the diversified portfolio is gives the best chance of success. Of course, to achieve this success rate, you have to put up with the additional day-to-day and year-to-year volatility that comes from having additional equity in the portfolio. For more on choosing an investment strategy, see our article Choosing an Expat Investment Strategy: Your Time Horizon Matters

Order of Investment Returns Matters

Short-term volatility is common for investors, as is the general rise of portfolios over the long run. Part of what determines if a portfolio will last for 30 years in retirement are the up and down periods encountered over that time, the order of investment returns, and when funds are withdrawn.

For example, having positive investment returns early in retirement and one negative year out of five in the last year can leave you with the same 5-year average if the return percentages are reversed.

However, you’ll end up with less money by withdrawing funds for retirement if the negative return year happens in the first year of the 5-year average. Why? Poor returns at the beginning of a retirement period combined with withdrawals quickly depletes the value of the portfolio and overwhelms its ability to recover, even when there are better returns later in the retirement period. For more details on this, see our article, Expat Investing: In Retirement, the Sequence of Returns Matters

Diversify and Save More Early

To combat that, a diversified portfolio is the best way to ensure your money lasts throughout retirement. You should also test your plan against actual returns during different historic and economic periods. Look at return sequences where the poor returns occur up front. Use Monte Carlo testing to generate thousands of potential return sequences and see how your plan stands up.

If you are a retiree in an emerging market, remember that emerging market equity and currency add another layer of volatility to expat portfolios. Plan accordingly.

Other things to do: Save more. Start early. Know your numbers, which means creating a financial plan that encompasses your unique situation and updating it frequently. Learn what successful long-term investing is all about. Learn to deal with market volatility. Create a lifestyle you can afford. Get help if you need it.

This article is a revised and updated version of an article that originally appeared on www.crevelingandcreveling.com.

Additional Resources

- Seven Things Expats Need to Know About Investing

- Expat Investing: In Retirement, the Sequence of Returns Matters

- Choosing an Expat Investment Strategy: Your Time Horizon Matters

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2023 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.