How Long Would Your Money Last If You Retired Today? An Expat Case Study

Creveling & Creveling protects its clients' privacy. The following is a fictitious example designed to demonstrate the type of financial decision-making required to achieve financial security and does not refer to any specific case.

Many working expatriates dream of the day when they can throw in the towel and retire on their savings, enjoying the benefits that an international lifestyle can bring without the hassle of having to work. But how do you know if you have enough to retire? How long would your money last if you retired today? Is there anything you can do to stretch your savings over the course of your retirement? To help answer these questions, consider the following case study.

Case Study: How Long Will This Expat Couple's Savings Last in Retirement?

Situation: Jim and Beth are expats considering early retirement. They are 55 years old, married, and living in Southeast Asia. They have saved over the years and have an estimated net worth of U.S. $2M, with no debt. Their financial assets include the following:

- A new investment condo with a market value of THB 15M (U.S. $500K), rented out with a gross yield of 5% and producing net annual cash flow after all expenses of THB 600K ($20K).

- An investment portfolio worth U.S. $1.5M consisting of $1.3M in U.S. taxable assets and $200K in a traditional U.S. individual retirement account (IRA). Overall, the portfolio is invested 55% in stocks, 30% in cash and fixed income, and 15% in gold. Total portfolio expenses average 1.25% per year, including fund expenses and trading commissions.

- U.S. Social Security benefits (Jim and Beth together) worth about $6,000 per year in current dollars when they are 67 years old.

Jim and Beth estimate that their lifestyle costs approximately U.S. $100K per year, including living expenses, housing, health insurance and medical costs, entertainment and dining out, gifts and charitable donations, and travel. They plan to keep the investment condo for about 10 years for its cash flow, and then hope to sell it at a small profit.

Analysis: Although U.S. $2.0M is not an insignificant amount of savings, unfortunately it may not be enough to support Jim and Beth in their expected lifestyle for the rest of their lives. Even assuming that the condo appreciates in value, that they can clear $600K from its sale in 10 years (after maintenance, closing costs, and taxes due), and that their other investments generally grow by 8.3% per year before portfolio costs, they stand a good chance of running out of money around the time they turn 84, leaving them with only a small income from the U.S.'s Social Security program.

In the early years of retirement, Jim and Beth may not realize that they do not have enough savings for their planned retirement, or at least as they have structured it currently. Rather deceptively, at first their net worth may continue to increase, giving them a false sense of security. However, due to inflation, the costs of their lifestyle will also increase.

In their current situation, the rate of increase of their costs is likely to be greater than the rate of increase in their net worth (which will be negatively impacted by their need to live off their investments). Eventually, their net worth will begin to fall in nominal terms as well. This could be a problem, as Jim and Beth may live far past age 84. For example, over half (50%) of healthy nonsmokers of their age live longer than 85 (men) and 88 (women), and 30% live longer than 91 (men) and 93 (women).

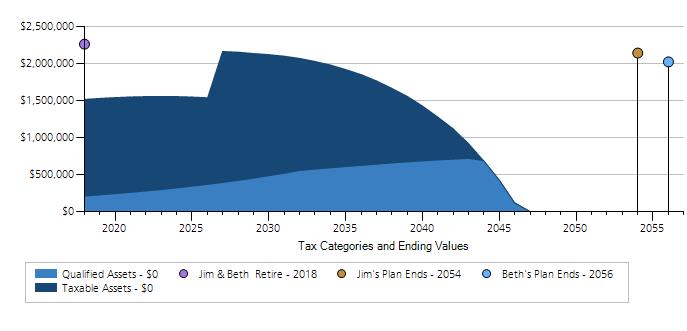

Jim and Beth’s Investments—Current Plan

Note: Condo sold in 2027, netting $600K after all costs; investments run out in 2047 when Jim and Beth are 84.

Solution: So how can Jim and Beth improve their chances of not outliving their savings without sacrificing their lifestyle?

- Revamp their investment portfolio. Jim and Beth could improve their investment portfolio in a number of areas to help it last longer. Right now, due to the large holding in gold and high fund expenses, the historical long-term return of their portfolio has averaged a real rate of return of just 3.13% per year after inflation and fees (8.33% nominal return – 3.95% inflation – 1.25% annual fees). In particular, they could consider an asset allocation with a better expected return per unit of risk (annual volatility), use low-cost index funds to cut the running costs, and use their IRA to hold any investments with high current yields to improve U.S. tax deferral. These simple moves alone would increase their expected real rate of return after inflation by 43% to perhaps 4.49% per year (8.69% nominal return – 3.95% inflation – 0.25% annual fees) and lower the annual volatility of the portfolio (risk). Compounded over many years, this move alone could help their savings last an additional six or seven years.

- Consider selling the condo now. The expected net yield and future appreciation of the condo may not be great enough to compensate Jim and Beth for the risk they are taking in having so much of their savings tied up in a single illiquid asset with an uncertain future cash flow stream and valuation. Jim and Beth may be able to improve on the longevity of their savings if they sell their condo and reallocate the proceeds to the revamped investment portfolio described in No. 1.

This is because, based on their estimated net rental yield and future expected sales price, the condo investment might achieve an internal rate of return (IRR) of just 6.3% (nominal) per year on average―including all income, costs, and price appreciation of the property. This represents a real rate of 2.36% after inflation, a figure significantly lower than the revamped portfolio and one that doesn't really compensate them for uncertainty embedded in many of their assumptions for the expected return of the condo investment. By selling the condo and redeploying the proceeds to the revamped portfolio, they could add a couple of more years to the life of their savings and, importantly, remove a considerable amount of uncertainty related to the condo’s future income and expenses.

- Supplement retirement costs with part-time income. Jim and Beth are relatively young and hopefully have many more years ahead of them. As highlighted in Jeff Rose's "7 Reasons to Work Part-Time in Retirement," there are a number of benefits to continuing to work, and not all of them are financial. Working part-time in retirement may be a great way for Jim and Beth to stay active and engaged, and in the meantime serve to stretch their savings further. If Jim and Beth take the above two steps and work part-time to earn just half of their annual expenditures (about $50,000 per year) for an additional 12 years, they are unlikely to run out of funds before they do years and may have a healthy safety margin in case they live longer.

Jim and Beth’s Investments—Revised Plan

Note: Jim and Beth move their investments to an improved asset allocation with lower-cost funds, sell their condo and redeploy the proceeds to their investment portfolio, and work part-time for an additional 12 years.

- Consider purchasing a low-cost annuity. At some point, Jim and Beth can consider purchasing a low-cost immediate fixed-income annuity. An immediate fixed-income annuity would require them to make an initial upfront payment to an insurance company, in exchange for which they would receive a stream of guaranteed income. The amount received would depend on the size of the initial payment, their age at the time of purchase, the interest rate level, and the income option that they choose (example: joint life income).

This type of annuity is different from the typical offshore pension schemes sold in that it is much lower in cost (the purchaser receives a larger payment), the payments are received immediately following the purchase, and there is no investment risk as the insurance company is contractually obligated to make fixed payments that are not linked to stock market performance. However, there can be counterparty risk if the insurance company runs into financial difficulty.

Jim and Beth are relatively young, and interest rates are at the low end of the cycle. So it may make sense to wait to purchase a low-cost immediate fixed-income annuity until they are a bit older and they can lock in a higher interest rate.

If they do decide to purchase a low-cost immediate fixed-income annuity, to maintain flexibility and hedge against inflation they will want to be sure to use only a portion of their savings. They will also want to be sure they purchase the annuity from a financially strong insurance company in a well-regulated jurisdiction such as the United States.

Summary

The above case study is intended to illustrate the type of analysis and decision-making that goes into considering whether you have saved enough to fully retire. Additionally, regardless of when and how much you have to retire, reorganizing your financial assets may allow you to add years to your savings’ expected life in retirement. Alternatively, planning to work part-time in retirement may provide you with unexpected nonfinancial as well as financial benefits.

This article is a revised and updated version of ones that have appeared previously on www.crevelingandcreveling.com.

Find more articles by Peggy Creveling, CFA, on Google+

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2018 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.