Expat Investment Advice: The Cost of Not Sticking with Your Investment Strategy in Volatile Markets

By Chad Creveling, CFA and Peggy Creveling, CFA

Volatile markets make for challenging times for investors. Wild swings in the market can trigger a roller coaster of emotion as investors understandably fear destruction in portfolio value and a loss of financial security. The news media, with eyeball-seeking urgency, stridency, and a sense of catastrophe, serves to heighten the fear and the impetus to take action.

Big institutional money managers can make things even worse by short selling/purchasing put options in an attempt to either insulate their positions or to profit by creating panic and the eventual capitulation of smaller, individual investors.

It's easy to succumb to fear and sell during and after market corrections in an effort to avoid further loss. Additionally, there is a sense that "savvy" investors make money actively buying and selling the markets. Despite having been decisively debunked, this type of attempt to time the market persists and unfortunately leads to an emotionally driven cycle of selling low and buying high.

Once drawn into this value-destroying cycle, many investors fail to realize the true cost to their ability to create long-term wealth.

The Cost of Bailing Out

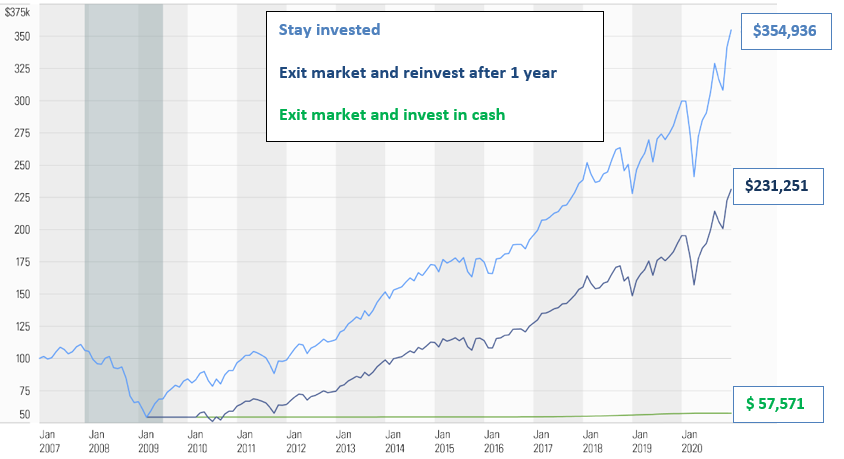

Morningstar, a leading research and investment management firm, attempted to quantify the cost of abandoning an investment strategy during times of volatility in the following chart.

The Importance of Staying Invested—Ending Wealth Values After a Market Decline

Source: Morningstar, Inc.

The chart shows a hypothetical USD 100,000 portfolio invested in the stock market from 2007 to 2020, a period that encompasses the last financial crisis and subsequent recovery. As the financial crisis unfolded, the market fell sharply, and at the bottom (known only in hindsight) in February 2009, the USD 100,000 was worth only USD 54,381. As the crisis and market decline unfolded rapidly, many investors were faced with steep losses in their portfolios before they knew it and had to make the decision to move to cash or risk a further decline. Since there was no sign of the crisis or market losses abating, the psychological pressure to do something to prevent further loss was immense.

For those who withstood that pressure and stayed with their investments, the market and the portfolio rebounded over the next 11 years to USD 351,936 at the end of 2020. For those who exited in February 2009 and stayed out of the markets for the next year, not believing the market recovery was genuine or rooted in economic reality, the portfolio rebounded to USD 231,251. And for those who threw in the towel, vowing never to go near the market again, they ended up with USD 57,571, or a permanent loss of USD 42,429 or -42%.

The difference in ending wealth based on different decisions made at the depth of the financial crisis and market decline is staggering. For those who stayed the course, their ending wealth was USD 123,685 more than those who sold and waited a year to get back in and USD 297,365 over those who sold at the bottom and never got back in.

Construct an Investment Strategy You Can Live With

Strong market rebounds tend to follow sharp market corrections, but the depth and duration of market corrections and recoveries can vary. The only constant is that the start of the decline and the subsequent recovery are unpredictable and known with certainty only in hindsight. While there are no easy answers, here are a few thoughts on living with market volatility and successful investing:

- Understand that volatility is a normal part of investing. It is impossible to predict and avoid. It must be endured if you plan to invest.

- Construct a portfolio that you can live with. This means constructing a portfolio that exhibits the amount of volatility that you can psychologically and financially bear. There is no point in being in an aggressive portfolio when a 5% drop in portfolio value causes so much concern that you consider selling to avoid further loss. You are in the wrong portfolio.

- Understand that returns on investments in the markets do not come evenly like earning interest on a deposit at a bank. They come in fits and starts, over a small number of days encountering temporary setbacks (sometimes significant), and only emerge for the investor in the long run.

- Use down periods in the market to add fresh funds. You will be entering at lower market levels (more attractive stock prices), which will help set you up for better longer-run returns.

- Use market volatility to tax-loss harvest or reduce concentrated positions with embedded capital gains (for example, company stock). Temporary losses in parts of the portfolio can be realized and used to offset gains in the concentrated position while improving the risk and return profile of the portfolio.

While devising a good investment strategy and sticking with it is generally the road to success in investing, like any rule there are times to break it. If your situation changes such that your current investment strategy no longer makes sense for you or it is clear that you are in the wrong portfolio, then a change is warranted. Ideally, this should occur when your situation changes, however, not at the depths of a financial crisis or market correction.

This article is a revised and updated version of one that had appeared previously on www.crevelingandcreveling.com.

Additional Resources

Expat Investment Advice: Tips to Deal with Market Volatility

Expat Investment Advice: Don't Chase Returns, Diversify Instead

Seven Things Expats Need to Know About Investing

About Creveling & Creveling Private Wealth Advisory

Creveling & Creveling is a private wealth advisory firm specializing in helping expatriates living in Thailand and throughout Southeast Asia build and preserve their wealth. The firm is a Registered Investment Adviser with the U.S. SEC and is licensed and regulated by the Thai SEC. Through a unique, integrated consulting approach, Creveling & Creveling is dedicated to helping clients cut through the financial intricacies of expat life, make better decisions with their money, and take the steps necessary to provide a more secure future.

Copyright © 2022 Creveling & Creveling Private Wealth Advisory, All rights reserved. The articles and writings are not recommendations or solicitations, and guest articles express the opinion of the author; which may or may not reflect the views of Creveling & Creveling.