Expat Investing: The Problem with Comparing Investment Returns

You hear it all the time: “My portfolio is up 15%!” or “My financial advisor is really clever—he’s getting me a 30% return!” Generally, this is harmless bragging, but it does tend to elicit envy and cause investors to question their own investment performance. Sometimes, it may lead someone to stray from a consistent, disciplined investment strategy appropriate for their unique situation.

When someone brags about their investment returns, there’s a good chance you’re not getting the full story. More important, there is no reason why your portfolio returns should be comparable to those of your bragging friend. Here are a couple of reasons why you shouldn’t pay too much attention to the supposed investment performance of others.

Your Friends Have No Idea What Their Returns Are

Measuring investment performance requires detailed tracking of all cash flows, positions, and accounts that make up the portfolio. Additionally, correctly calculating performance numbers is a complex task that requires specialized software. It’s not a matter of simply dividing the portfolio’s ending value by the beginning value.

The typical expat household has numerous investment and bank accounts—some have more than 15, often in multiple currencies. Given time constraints and the need for specialized software, it’s unlikely the average person can keep track of all of their accounts, let alone complete the complex calculations required for accurate performance reporting on their aggregate account position.

Most people citing return figures are getting the numbers from a financial statement, or in some cases from a financial advisor. These figures should be taken with a grain of salt. Typically, some cherry picking is going on. The number may be for only one position or one account in the overall portfolio, rather than for the entire investment portfolio. Additionally, you can’t be sure you’re even talking about the same period. You may be looking at year-to-date performance, while your colleague is talking about the most recent quarter.

Additionally, the currency that a return is quoted in matters—a lot. Comparing a USD return to, say, a GBP return is like comparing apples to oranges—there is simply no basis for equivalence. Returns must be quoted in the same currency.

A qualified investment manager will provide a properly calculated performance figure for the funds you have invested with them. But when it comes to other people’s investments, you don’t know if the funds with that manager represent the entire portfolio or only a portion of their portfolio. You also don’t know whether the returns with a particular investment manager are for a diversified strategy or simply one segment of a greater number of global asset classes.

Different Asset Allocations

Your portfolio’s asset allocation is one of the biggest contributors to your long-run investment returns and the short- and long-term volatility you experience. There is not a one-size-fits-all asset allocation that is appropriate for everyone. A 60-year-old expat planning to retire in Canada is going to have a very different (or should have) asset allocation than a 40-year-old living and working in Thailand. Different asset allocations mean different performance numbers.

Different Risk Levels

One of the key factors driving the asset allocation decision is the portfolio’s risk level. A 55-year-old nearing retirement is going to have a very different risk level than a long-retired 90-year-old or a 35-year-old just starting out with no obligations. (If the 90-year-old’s portfolio starts “beating” the other two portfolios, there’s a problem.)

Different Portfolio Cash Flows

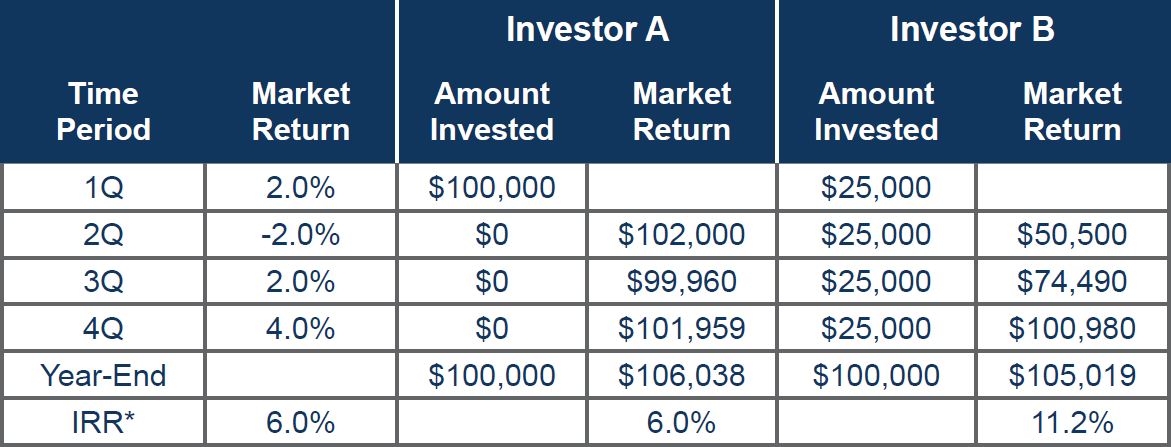

Over any investment period, cash added to or taken from the portfolio can have a big effect on returns, particularly in a volatile market. A person who had all their money invested at the beginning of the year is going to have a different return than the investor who added money each quarter. Consider the example in the table below:

How Returns Differ: USD 100,000 Invested at Once or over Time

Investor A invests USD 100,000 at the beginning of the year, and Investor B invests USD 25,000 per quarter. Both invest in the same portfolio allocation, yet as the table shows, at year’s end, they’ll end up with very different rates of return.

*IRR = Internal rate of return.

Different Performance Measures

As mentioned earlier, measuring investment performance is complicated. In the investment profession, there are typically two main ways to calculate investment performance. One is called the time-weighted return (TWR), and the other is a dollar-weighted return (DWR). The TWR strips out the impact of cash flows on the portfolio and measures the compounded return as if one dollar were invested over the investment period. This return calculation most accurately measures the results of a particular investment strategy or manager since they cannot control for when investors add or subtract money from a fund or portfolio. The TWR is the performance number typically reported by a mutual fund, investment manager, or broker.

It is important to note, however, this is not the investor’s return unless the investor was fully invested at the beginning of the investment period and did not add or withdraw any money from the fund or portfolio. The accurate measure of an investor’s return is the DWR, which accounts for the timing of cash flows in and out of the portfolio and measures the return on the average dollar invested. This number can vary greatly from the TWR reported by the fund or portfolio manager, especially in volatile markets and when there are significant cash flows during the investment period.

The next time someone starts boasting about performance numbers, you might want to ask whether they are talking about the manager’s time-weighted return or their own dollar-weighted return.

Devise an Appropriate Benchmark and Stick to It

Performance measurement is important to ensure that your portfolio is performing in line with the objectives, risk levels, and other parameters you have set for it. It is not particularly useful as a means of keeping score, competing with your colleagues, or bolstering esteem. For the reasons cited above, it is very difficult to compare investment performance numbers for two different investors. To stay on track to achieve your goals, devise an investment portfolio appropriate for your unique situation, choose an appropriate benchmark, track your portfolio’s performance against that benchmark, and try not to get drawn into the next intra-office bragging session.

This article is a revised and updated version of one that had appeared previously on www.crevelingandcreveling.com.