How Much Do You Need to Retire? An Expat Case Study

Creveling & Creveling protects its clients’ privacy. The following is a fictitious example designed to demonstrate the type of financial decision-making required to achieve financial security and does not refer to any specific case.

The Situation

John is a single American expatriate, age 45, living and working in Bangkok. Until recently, he has not been in a position to save and has accumulated only $100,000 for future financial goals such as retirement. Now that he can save, he wants to know how much he will need to retire safely and to avoid the risk that he will run out of money before he dies. He is not sure where he will retire, but he would like to have the flexibility to return to the U.S., if needed.

The Approach

For many expats, the proverbial million-dollar (or even multimillion-dollar) question is how much is needed for retirement. Of course, without a crystal ball, there’s no way of knowing for sure. But in making a few educated estimates and calculations, you can come up with ballpark estimates of how much you should be saving and investing for your retirement. In John’s case, here are some of the things that he will need to consider:

- How much he plans to spend annually in retirement

- How many years he'll be retired

- How much he can save each year before retirement

What John Estimates

How much will he spend annually in retirement? This number can be a hard one to pin down, especially as retirement is many years away and John is not sure where in the world he will end up. John can start by calculating what it costs to maintain his current lifestyle. He will need to add all costs that he will pay for in retirement, even those that his employer may currently pay (in John’s case, housing, health care, transportation, and some international travel). Then he should calculate an alternative location, preferably one at the opposite end of the spectrum in terms of cost. John calculates that his lifestyle costs THB 2.55 million (about USD 75,000) in current costs in Bangkok. He estimates that it may cost more (or perhaps less) to maintain his lifestyle if he retires in another country or elsewhere in Thailand.

How many years will John be in retirement? As a nonsmoker, John’s life expectancy is 86 years. But before using 86 as a basis for his calculation, John needs to remember that he has a 50% chance of living longer than his life expectancy. Unless he wants to run a 50% chance of outliving his money, he will need to plan for the fact that he may live longer. As he is in good health, is physically fit, and has access to good-quality medical care, John decides to use a target age of 91 years. This number, combined with his target retirement age of 65, means that John wants to fund at least 27 years in retirement from his savings.

How much can he save each year? John’s current after-tax salary and bonus total THB 4 million (about USD 117,500). Since his lifestyle costs less than that, he plans to save THB 1.45 million a year (about USD 42,500). He plans to invest his savings in a low-cost, moderately aggressive investment portfolio (35% fixed income and 65% equity and alternative investments) made up of exchange-traded funds (ETFs) and index funds.

Is It Enough?

If John sticks to his plan and diligently saves and invests as described over the next 20 years, after adjusting for ETF and index fund fees, he might earn on average a pretax nominal return of 9% per year (or 5% “real” rate of return after inflation). Assuming his savings can earn this percentage year in and year out until he retires at age 65, his retirement portfolio would be worth about $3.0 million in future U.S. dollars. Meanwhile, using a long-term inflation estimate of 4.0% per year, he estimates that his current living expenses of USD 75,000 will have inflated to about USD 164,000 in future dollars when he retires.

At first glance, USD 3.0 million would seem to be enough to cover John’s retirement living expenses. For example, even if he switches his portfolio to a lower-risk allocation in retirement, and considering that he’ll be paying U.S. tax on his investment earnings and that his expenses will continue to grow with inflation, a spreadsheet calculation suggests that John would have USD 453,600 in future dollars (USD 24,000 current) left over when his “plan ends” at age 91. Since he does not plan to leave an inheritance to anyone, at first glance, this might seem to be a reasonable plan:

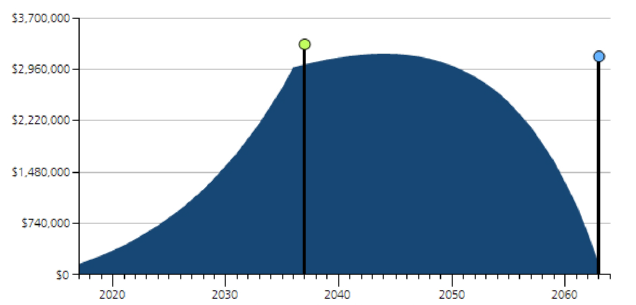

John’s Estimated Retirement Savings, Pre and Post Retirement

Average Historic Returns

John retires in 2037 at age 65, and dies in 2063 at age 91 with a small amount of money left.

Source: MGP, C&C estimates.

But what if something unexpected happens? Unfortunately, the world does not operate like a spreadsheet―something unexpected always happens. Importantly, in the above scenario, John has virtually no safety margin. And also importantly, unlike an Excel spreadsheet calculation, investment returns are not smooth. Volatile investment markets will result in a lower effective rate of return than the simple average used in Excel calculations. Even if things mostly go as planned, market volatility alone could create a situation where John runs out of money.

Additionally, if John is unlucky, a number of other things could go wrong. The markets may do worse than average over the next 20 years, or perhaps he simply won’t save as much as expected. His expenses could be higher than anticipated for items such as health care. There’s also a reasonable chance that he could simply live longer than anticipated and outlive his money. For example, 30% of the nonsmoking male population is projected to live past age 91. He could also end up retiring in a bad year (as in 2008) when markets are down.

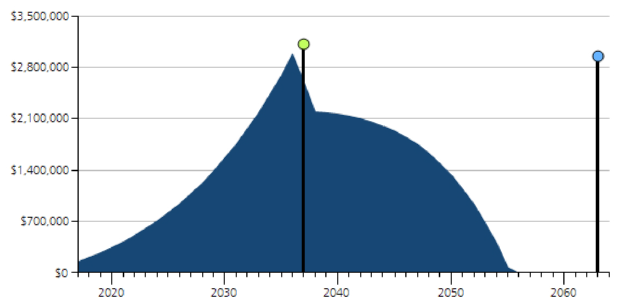

John’s Estimated Retirement Savings, Pre and Post Retirement

Retires in Bear Market and Runs Out of Money

Scenario: John retires in 2037 at age 65 in a bear market and runs out of money in 2055 at age 83.

Source: MGP, C&C estimates.

In fact, stress-testing John’s situation under a variety of market conditions shows that his chances of running out of money before he dies are more than 40%.

Some Possible Solutions

Saving more per year at this point may be difficult for John since he is already planning to invest a significant amount of his salary and benefits. But there are other ways that he can improve his chances of not running out of money in retirement. Some of the areas that are worth looking into include:

- Working longer/saving more: Assuming he is physically able to, if John works an additional five years and retires at age 70, he will considerably improve his chances of not running out of money. Those additional years of adding to, instead of subtracting from, his portfolio make a substantial difference―his safety margin improves dramatically. If he retires at 70, his chances of running out of funds―even if he maintains his current lifestyle―are low.

- Cutting his expected costs by retiring in a lower-cost place: While John used to think that living in Bangkok is inexpensive, he has noticed that his living expenses in the city have inflated in recent years. Closer to retirement, he may want to re-evaluate whether it could make sense to retire in a place that costs less than Bangkok. But even then he needs to be careful: Despite all the “retire overseas” articles that flood the internet, this decision is not a no-brainer. Just as has happened in Bangkok, higher local inflation in current low-cost places may make those locales more costly during his retirement. Also, one of John’s likely major expenses in retirement—health care—may not be insurable outside the U.S. Much can change over the next 20 years, and John will want to re-evaluate his options closer to retirement.

- Contributing to tax-deferred or tax-free investment accounts: Depending on his situation, as a U.S. taxpayer John may be able to make his investment portfolio last longer by shielding some of his investment returns from U.S. tax by making annual contributions to an individual retirement account (IRA) or Roth IRA. To decide whether this is an option for him, he will first have to calculate whether he qualifies to contribute. If he does qualify, he should analyze whether he is likely to be better off over the long run making contributions to these types of accounts.

- Consider purchasing an inexpensive immediate fixed annuity in retirement: Annuities are sold by insurance companies. For a lump sum, the purchaser can buy a future cash flow stream that will end at their death. John will need to be careful in considering this option. An immediate fixed annuity indexed to inflation and purchased in retirement from a low-cost provider such as Vanguard or Fidelity may be one way to boost his retirement income. However, purchasing an expensive variable annuity sold in the offshore market today should be avoided for a number of reasons, including high costs, poor transparency, and U.S. tax issues. The decision to buy an immediate fixed annuity should be made closer to retirement, and John will want to carefully consider his situation and what’s on the market at that time.

In conclusion, the above case study is intended to illustrate the type of analysis and decision-making that goes into retirement financial planning. While John has waited until relatively late to start saving, if he is clear about what is achievable and can create and conscientiously implement a realistic savings and investment plan, he will be well on the way toward achieving his goals.

This article is a revised and updated version of one that appeared previously on www.crevelingandcreveling.com.